Stryker Corporation (SYK-US)

Company Basics

Executive Summary

Stryker Corporation is a global leader in medical technologies, specializing in MedSurg, Neurotechnology, Orthopaedics, and Spine. This report analyzes the key drivers of Stryker's performance, competitive strategy, and differentiation factors.

Company Overview

Business Segments: Stryker operates in four main segments: MedSurg, Neurotechnology, Orthopaedics, and Spine. In 2023, MedSurg and Neurotechnology accounted for 58% of sales, while Orthopaedics and Spine accounted for 42%.

Global Reach: Stryker impacts over 150 million patients annually and has a presence in approximately 75 countries

Innovation and R&D: The company spent $1.4 billion on R&D in 2023 and owns over 12,900 patents globally. Recent product launches include the Prime Connect Stretcher, Xpedition Powered Stair Chair, and Neptune S Waste Management System.

Revenue Drivers

Organic Growth: Stryker achieved over 11% organic sales growth in 2023, driven by innovation and market expansion. International sales, particularly in emerging markets, contributed significantly to this growth.

Acquisitions: The company has made over 50 acquisitions in the last 10 years, focusing on both organic and non-organic innovation. However, some analysts have raised concerns about the company overpaying for these acquisitions, which could impact future growth.

Shift in Site of Care: Stryker is well-positioned to benefit from the trend of procedures shifting to ambulatory surgery centers (ASCs), which is a growing market segment.

Competitive Strategy

Innovation: Stryker's competitive edge is largely driven by its innovative products and technologies. The company invests heavily in R&D to stay ahead in the market.

Globalization: Stryker's international presence and double-digit organic sales growth in international markets are key to its competitive strategy. The U.S. market still accounts for over 70% of sales, but international growth is a significant focus.

Corporate Responsibility: Stryker's commitment to corporate responsibility, including environmental health, education, and community support, enhances its brand and attracts socially conscious investors and customers.

Differentiation

Product Portfolio: Stryker's diverse and innovative product portfolio across multiple healthcare segments differentiates it from competitors. The company's ability to provide game-changing technologies for the continuum of patient care sets it apart.

ESG Performance: Stryker's strong Environmental, Social, and Governance (ESG) performance, including renewable energy initiatives and diverse board composition, is a differentiation factor. The company reports its greenhouse gas emissions and reduction initiatives through CDP and aligns its emissions goals with the 1.5-degree threshold for science-based targets.

Customer and Employee Engagement: Stryker's engagement with customers and employees through initiatives like Climate Week Town Hall and embedding Corporate Responsibility Champions across the company enhances its reputation and loyalty.

Analyst Views and Market Expectations

Price Targets: Analysts have set an average 12-month price target of $381.35 for SYK, with a high estimate of $405 and a low estimate of $341.35.

Concerns Over Acquisitions: Some analysts, like those at Spruce Point Capital Management, have raised concerns about Stryker overpaying for acquisitions, which could lead to a downside risk of 35% to 75% or a share price range of $67.00 to $174.50.

Positive Outlook: Despite these concerns, many analysts remain positive about Stryker's long-term prospects due to its strong innovation pipeline, global expansion, and commitment to ESG.

Financial Performance

Revenue: Stryker reported $20.5 billion in global sales for 2023, with an 11% organic sales growth.

R&D Spend: The company spent $1.2 billion on R&D in 2023, reflecting its commitment to innovation.

Simple Operating Model

To build a simple operating model for Stryker Corporation (NYSE: SYK), here are some key points to consider based on the available data:

Organic Volume & Pricing Trends

Over the past few years, Stryker has demonstrated strong organic sales growth driven by both volume and pricing.

Recent Trends: In Q1 2024, organic net sales grew by 10.0%, with 9.3% from increased unit volume and 0.7% from higher prices. For the full year 2023, organic net sales increased by 11.5%, with 10.9% from increased unit volume and 0.6% from higher prices.

Historical Margin Trends & Incremental Margins

Stryker has maintained robust margin profiles.

Operating Income Margin: In Q1 2024, the reported operating income margin was 18.5%, while the adjusted operating income margin was 21.9%. For the full year 2023, the reported operating income margin was 19.0%, and the adjusted operating income margin was 24.2%.

Incremental Margins: The company has shown the ability to expand margins. For instance, in Q2 2024, the adjusted operating income margin increased by 30 bps to 24.6%. This suggests that Stryker can convert sales growth into higher profitability.

Major Capital Allocation Decisions

Stryker has been active in strategic acquisitions and investments.

Acquisitions: Recent acquisitions include Arlon and Moly Surgical, which have enhanced Stryker's portfolio and contributed to its growth.

Research and Development: Stryker consistently invests in R&D to drive innovation and maintain its competitive edge in the medical technology sector.

Share Buybacks and Dividends: While not explicitly mentioned in the sources, Stryker, like many other large-cap companies, likely allocates capital to share buybacks and dividend payments to return value to shareholders.

Key Drivers and Relationships Between Revenue, EBITDA, and Earnings Per Share

Revenue Drivers

Segment Performance: Revenue growth is driven by strong performances in the MedSurg and Neurotechnology, and Orthopaedics and Spine segments. For example, in Q1 2024, MedSurg and Neurotechnology saw an 11.5% increase in net sales, while Orthopaedics and Spine saw a 7.5% increase.

Geographic Performance: Stryker benefits from a global presence, with growth in both U.S. and international markets.

EBITDA and Margin Relationships

Operating Leverage: Stryker's ability to maintain and expand its operating margins indicates strong operating leverage. As sales grow, the company can convert a significant portion of this growth into higher EBITDA and earnings.

Adjusted vs. Reported Margins: The difference between reported and adjusted margins suggests that Stryker manages certain one-time or non-recurring items effectively, which helps in maintaining a stable and high adjusted margin profile.

Earnings Per Share (EPS)

EPS Growth: Adjusted EPS has shown consistent growth, with a 16.8% increase in Q1 2024 and a 10.6% increase in Q2 2024. Full-year 2024 adjusted EPS is expected to be in the range of $11.90 to $12.10.

Drivers of EPS Growth: EPS growth is driven by a combination of revenue growth, margin expansion, and effective management of operating expenses.

Fundamental Drivers

To identify the top 3 fundamental drivers for Stryker, we need to analyze several key aspects of the company's business model, financial performance, and market dynamics.

Key Business Segments and Revenue Contribution

Stryker is a broadly diversified medical technology company with several key business segments. Here is a breakdown of the major segments based on the available data:

Orthopaedics: This includes joints (knees, hips, extremities), trauma, and spine. Orthopaedic sales were $2,446.8 million in the third quarter of 2023, representing a significant portion of Stryker's revenue. For the first nine months of 2023, orthopedic sales were $7,437.1 million, showing a 9.5% year-over-year growth.

Neurotechnology: This segment includes neuro powered instruments, neurovascular, and craniomaxillofacial products. While specific quarterly figures are not provided, neurotechnology is one of the three key hospital service lines Stryker focuses on.

Specialty Surgery: This includes endoscopy, instruments, and sustainability solutions. These segments also contribute significantly to Stryker's revenue, though specific percentages are not detailed in the recent reports.

Key Profit Drivers in the Operating Model

Product Innovation and New Product Launches

Stryker's consistent cadence of new products is a key driver of its high-end performance in the medtech industry. New products, such as the Pangea plating system and Mako Spine, are expected to drive significant sales growth. The company's focus on procedural simplification and workflow flexibility through technologies like computer-assisted surgery and robotic procedures is crucial for maintaining market leadership.

Decentralized Business Units and Sales Force Execution

Stryker's decentralized business units, which include dedicated sales, business development, marketing, and research & development functions, allow for rapid identification and addressing of customer needs. This organizational structure is pivotal in driving market share gains and category leadership.

International Growth and Market Expansion

International growth, particularly in regions like Australia, Canada, and emerging markets, is another significant driver. Stryker's ability to leverage its broad product portfolio and services to capture market share in both developed and emerging markets is essential for sustained growth.

Bull vs Bear Case Arguments

As of this writing on Nov. 21, 2024 here is the breakdown of 26 sell-side ratings

The average target price from sell-side ratings is $402.24 and the median is $405.00

Bull Case

Innovation and New Product Launches: Stryker's continuous introduction of new products and technologies, such as the Mako robotic system and the upcoming Pangea plating system, positions the company for sustained growth and market leadership.

Strong International Growth: The company's success in international markets, particularly in emerging regions, provides a significant growth opportunity.

Decentralized Business Model: The decentralized structure allows for agile response to market needs, driving market share gains and category leadership.

Bear Case

Market Competition: The medical device industry is highly competitive, and Stryker faces competition from other major players, which could impact market share and pricing power.

Economic and Regulatory Risks**: Economic downturns or changes in regulatory environments could affect hospital spending and procedural volumes, impacting Stryker's sales and profitability.

Integration Risks from Acquisitions: While acquisitions have been a key growth strategy for Stryker, integrating new companies and technologies can be challenging and may not always yield expected results.

In summary, Stryker's fundamental drivers include its robust product innovation, decentralized business model, and strong international growth. The bull case is supported by the company's innovative product pipeline, successful international expansion, and effective business model. The bear case highlights potential risks from market competition, economic and regulatory changes, and integration challenges from acquisitions.

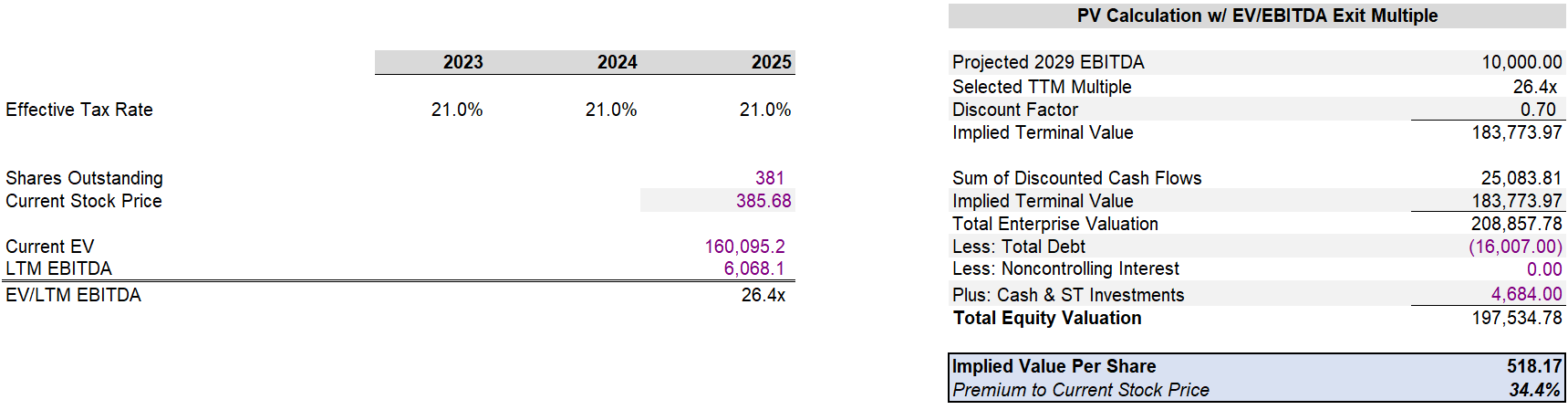

Build Operational DCF

Base Scenario

Assumptions:

Discount Rate:7.5%

Effective Tax Rate: 21%

Rev growth: 10% decreasing towards 4.5%

Terminal year growth rate: 4%

EBITDA margin: ~26%

Annual Incremental Working Capital: $350M

Bull Scenario

Assumptions:

Discount Rate: 6.0%

Effective Tax Rate: 21%

Rev growth: 13% decreasing towards 6%

Terminal year growth rate: 5.5%

EBITDA margin: ~30%

Annual Incremental Working Capital: $200M

Bear Scenario

Assumptions:

Discount Rate:9.0%

Effective Tax Rate: 26%

Rev growth: 9% decreasing towards 2.5%

Terminal year growth rate: 2.5%

EBITDA margin: ~18%

Annual Incremental Working Capital: $550M

Comparison to Current Stock Price

As of the latest data, Stryker's stock price is around $385 per share. The estimates provided here outline a highly variable range of outcomes based on moderate changes to the profitability and growth of the business.

Current Stock “Narrative”

To gain a comprehensive understanding of the current stock narrative for Stryker Corporation (SYK), here are some key points derived from recent reports, earnings calls, and other investor-related communications:

Financial Performance and Growth

Stryker has demonstrated strong financial performance, with earnings growing by 27.3% over the past year. The company is forecasted to continue this growth, with earnings expected to increase by 10.84% per year.

The recent earnings report showed a significant drop in the stock price due to the company's results, but overall, the stock has performed well, exceeding both the US Medical Equipment industry and the US market over the past year.

Management's Message

Top management emphasizes the company's focus on organic growth, calculated acquisitions, and innovation. This strategy is highlighted as a key driver for future success, indicating that Stryker is committed to expanding its product portfolio and market presence through both internal development and strategic acquisitions.

Earnings Calls and Reports

In recent earnings calls, management has been bullish on the company's prospects, highlighting the success of new product launches, such as the Mako shoulder and spine systems. These launches are expected to contribute to future growth.

The company has also reassured investors about its ability to manage debt sensibly, which has been a point of discussion in recent earnings calls and reports.

Investor Day Presentations and Conference Webcasts

Stryker's presentations often emphasize the company's commitment to innovation and its robust pipeline of new products. This includes advancements in surgical technologies and other medical devices, which are seen as key drivers for long-term growth.

Management has also highlighted the company's dividend growth, with Stryker being described as a "dividend growth powerhouse." The recent dividend announcement of $0.80 per share reflects the company's commitment to returning value to shareholders.

Market and Industry Position

Stryker's stock has shown relatively stable price volatility compared to the broader market and the medical equipment industry. This stability, combined with its strong past performance, suggests that the company is viewed as a reliable investment within its sector.

Insider Activity and Analyst Sentiment

There has been significant insider selling over the past three months, which might raise some concerns. However, analysts remain generally bullish on the stock after recent results, indicating confidence in the company's future prospects.

In summary, the current narrative around Stryker's stock is positive, with a focus on the company's strong financial performance, innovative product pipeline, and stable market position. Management's emphasis on organic growth, strategic acquisitions, and dividend growth further supports the optimistic outlook from analysts and investors.

Comparative Competitive Analysis

To conduct a comparative competitor analysis for Stryker, it's important to focus on the specific markets and segments where Stryker operates, as Unum Group is not a direct competitor to Stryker but rather a provider of different services.

Stryker's Competitors and Market Analysis

Key Competitors

Stryker operates in several medical device markets, including orthopedic devices, neurotechnology, and surgical equipment. Here are some of its key competitors in different segments:

Orthopedic Devices: Smith & Nephew, Arthrex, ConMed Linvatec, DePuy Synthes, and NuVasive.

Neuromodulation, Neurovascular, and Neurosurgical Devices: Medtronic, Boston Scientific, and St. Jude Medical (Abbott).

Surgical Equipment: Medtronic, Ethicon, and Olympus.

Organic Growth and Margins

Stryker: Stryker has demonstrated robust organic growth through its aggressive M&A strategy and strong product offerings. For example, in 2019, Stryker's net sales grew by 9.4% compared to the previous year, with significant growth in the Neurotechnology and Spine segments (19.2% and 31.1% respectively).

Competitors:

Medtronic: Known for its strong presence in various medical device segments, Medtronic often competes closely with Stryker, especially in neurovascular and spine markets. Medtronic's growth can be steady but may vary by segment.

Smith & Nephew: This company has a strong presence in arthroscopy and orthopedic devices. While it competes effectively in certain segments like RF probes and hip arthroscopy, its overall growth may not match Stryker's aggressive expansion through acquisitions.

Boston Scientific: Boston Scientific maintains a strong position in spinal cord stimulators and other neurovascular devices. Its growth is often driven by innovative products and strategic acquisitions.

Efficiency Metrics

Stryker: Stryker's efficiency is often measured by its ability to integrate acquired companies and technologies, as well as its investment in R&D. For instance, Stryker invested over $225 million in R&D facilities in Ireland to bolster its neurovascular and other technologies.

Competitors:

Medtronic: Medtronic also invests heavily in R&D and has a strong track record of integrating acquired companies. Its efficiency metrics are often aligned with its market leadership in various segments.

Smith & Nephew: This company focuses on innovation and has made strategic acquisitions to enhance its product portfolio. However, its efficiency might be more variable compared to Stryker's consistent growth through acquisitions.

Performance Comparison

Stryker: Stryker has been outperforming many of its peers in terms of sales growth and market expansion. Its strategic acquisitions, such as the purchase of Wright Medical, have significantly enhanced its market position in extremities and biologics.

Competitors: While competitors like Medtronic and Boston Scientific are strong players, Stryker's aggressive M&A strategy and focus on innovation have allowed it to maintain a competitive edge. Smith & Nephew and other competitors may underperform in certain segments where Stryker has a stronger presence.

Opportunities and Threats

Opportunities:

Stryker's continued investment in R&D and its ability to integrate new technologies and companies provide significant opportunities for growth.

Expanding into emerging markets and segments like minimally invasive spine (MIS) solutions can further enhance its market share.

Threats:

Regulatory challenges, such as the anticompetitive investigations surrounding the Wright Medical acquisition, can delay or complicate expansion plans.

Intense competition in the medical device market, particularly from companies like Medtronic and Boston Scientific, can pose challenges to maintaining market share and pricing power.

In summary, Stryker's competitive advantage lies in its aggressive M&A strategy, strong R&D investments, and its ability to integrate new technologies and companies. While it faces intense competition, Stryker generally outperforms its peers in terms of growth and market expansion. However, regulatory challenges and competitive pressures remain as potential threats.

Catalysts & POV

To develop a point of view on the upcoming catalysts for Stryker Corporation (NYSE: SYK) and assess any divergent views using the PSUC (Probability of Success Uncertainty Coefficient) framework, here are the key catalysts and their associated market embedded views:

Upcoming Catalysts

Mako Shoulder and Spine Launches

Market Embedded View: The launch of Mako shoulder and spine applications in 2024 is expected to be a major catalyst for Stryker's stock price and long-term success. Analysts believe these launches will leverage Stryker's existing installed base and expand its market reach.

Assessment: Given the successful track record of Mako in hip and knee replacements, there is a high probability of success for these new applications. However, the initial launch in 2024 may not generate tremendous revenue immediately, but it is crucial for long-term growth.

PSUC Analysis: Assuming a 15% upside on successful adoption and integration (win %) and a 5% downside if the adoption is slower than expected (loss %), the PSUC would be \((1 - (15 / (15 + 5))) = 0.75\) or 75%. This suggests a relatively high confidence in the success of these launches.

Organic Revenue Growth and Earnings Projections

Market Embedded View: Stryker is expected to achieve 9-10% organic revenue growth in FY24, with adjusted EPS growth of 12% at the midpoint. This growth is driven by strong customer demand, supply chain improvements, and a backlog of orthopedic procedures.

Assessment: The market seems optimistic about these projections, given the company's historical performance and current trends. However, there are risks such as hospital staffing issues and economic downturns that could impact these projections.

PSUC Analysis: Assuming a 10% upside on meeting or exceeding these projections (win %) and a 7% downside if the projections are missed (loss %), the PSUC would be \((1 - (10 / (10 + 7))) = 0.71\) or 71%. This indicates a moderate to high confidence in achieving these growth targets.

Strategic Acquisitions

Market Embedded View: Stryker's recent and planned acquisitions, such as Vertos Medical Inc., care.ai, and MOLLI Surgical Inc., are expected to enhance revenue streams and expand its product offerings.

Assessment: While these acquisitions are seen as positive catalysts, they also come with integration risks and potential impacts on margins. The market's optimism might be slightly overestimated given these risks.

PSUC Analysis: Assuming a 12% upside on successful integration and revenue growth from these acquisitions (win %) and a 10% downside if integration challenges arise (loss %), the PSUC would be \((1 - (12 / (12 + 10))) = 0.69\) or 69%. This suggests a moderate confidence in the success of these acquisitions, with a slightly lower PSUC than the market's embedded view.

Cost Reduction Strategies and Product Launches

Market Embedded View: Stryker's cost-cutting measures and new product launches, such as the LifePak 35 monitor/defibrillator and Pange Plating system, are expected to contribute to its growth.

Assessment: These initiatives are generally seen as positive, but their impact might be more incremental rather than transformative.

PSUC Analysis: Assuming a 5% upside on successful implementation of these strategies (win %) and a 3% downside if they do not yield expected results (loss %), the PSUC would be \((1 - (5 / (5 + 3))) = 0.62\) or 62%. This indicates a moderate confidence in these initiatives, slightly lower than the market's expectations.

Divergent Views

Integration Risks of Acquisitions

While the market is optimistic about Stryker's acquisition strategy, there is a potential for integration challenges that could pressure margins and impact the company's financial performance. This risk might be underappreciated by the market.

PSUC Adjustment: Given the potential for integration issues, the PSUC for successful integration might be lower than the market's embedded view, suggesting a more cautious stance.

Economic and Healthcare Industry Risks

The market's projections for Stryker's growth might not fully account for broader economic risks, such as inflationary pressures and fluctuations in exchange rates, which could impact the company's operations and margins.

PSUC Adjustment: Considering these external risks, the PSUC for achieving the projected growth could be lower than the market's expectations, indicating a need for a more conservative outlook.

In summary, while the market is generally optimistic about Stryker's upcoming catalysts, there are areas where a more cautious or divergent view might be warranted. Specifically, the integration risks associated with acquisitions and the potential impact of broader economic and healthcare industry risks could adjust the PSUC downward from the market's embedded views.

Scenario Planning

To develop a comprehensive bull, base, and bear case scenario for Stryker Corporation (SYK), we need to consider various factors including the company's financial health, market position, industry trends, and analyst opinions.

Bull Case

Assumptions:

Stryker continues to innovate and expand its product portfolio in the medical technology sector, driving strong demand and market share growth.

The company successfully integrates recent acquisitions, leading to synergies and increased efficiency.

Insiders' confidence, as indicated by recent buying activity, translates into sustained performance and growth.

The global healthcare market experiences robust growth, fueled by an aging population and increasing healthcare spending.

Stock Value:

Based on the consensus price target and considering additional upside potential due to strong innovation and market expansion, the bull case stock value could be around $420-$450.

Probability:

Given the positive analyst sentiment and the company's strong financial position, assign a probability of 40% to the bull case.

Base Case

Assumptions:

Stryker performs in line with current analyst expectations, maintaining its market position and financial health.

The company continues to invest in research and development, supporting steady growth but without significant breakthroughs.

The global healthcare market grows at a moderate pace, supporting steady demand for Stryker's products.

Insider transactions remain neutral, reflecting stable company performance.

Stock Value:

The base case aligns with the current consensus price target of $379.37.

Probability:

This scenario is the most likely given the current analyst consensus, so assign a probability of 50%.

Bear Case

Assumptions:

Stryker faces increased competition in the medical technology sector, leading to reduced market share and pricing pressure.

The company encounters integration challenges with recent acquisitions, resulting in higher-than-expected costs and reduced efficiency.

Global economic downturns or healthcare budget constraints reduce demand for Stryker's products.

Insider selling increases, indicating potential concerns about the company's future outlook.

Stock Value:

Considering potential downsides, the bear case stock value could be around $320-$340.

Probability:

Given the potential risks and the cautious approach of some analysts, assign a probability of 10% to the bear case.

Probability Tree Value

To calculate the probability tree value, we multiply each scenario's stock value by its assigned probability and sum these values:

EV = P(Bull) + P(Base) + P(Bear)

EV = (0.4 * $425) + (0.5 * $379) + (0.1 * $330)

EV = $170 + $189.685 + $33

EV = $392.685

Comparison to Current Stock Price

As of the recent data, the stock price of Stryker is around $385. The probability tree value ($392.685) is higher than the current stock price ($385.50), suggesting that, based on these scenarios, the stock might be undervalued.

Reward vs. Risk Asymmetry

Reward: The potential upside in the bull case is modest, with a possible gain of $7-$10 from the current price.

Risk: The potential downside in the bear case is about $50 from the current price.

The reward potential is less than the risk potential, indicating an asymmetry that favors the downside. This suggests that, based on these scenarios, investing in Stryker could offer more potential reward than risk, although this analysis is subject to the assumptions and probabilities assigned.