Does the Soaring National Debt Matter?

I completed my MBA at Emory‘s Goizueta Business School in Atlanta this month. In April 2024, The Adam Smith Society on campus invited Brian Riedl to speak about some of this current focus areas.

Brian is a senior fellow at the Manhattan Institute, focusing on budget, tax, and economic policy. Previously, he worked as an economic advisor for Senator Rob Portman (R-OH) and as staff director of the U.S. Senate Finance Subcommittee on Fiscal Responsibility and Economic Growth. Before that, Brian spent a decade as lead research fellow on federal budget and spending policy at the Heritage Foundation. Brian also served as a policy advisor for Marco Rubio’s 2016 presidential campaign and was the lead architect of the 10-year deficit-reduction plan for Mitt Romney’s 2012 presidential campaign. Brian has published nearly 600 studies and articles on federal spending, taxes, deficits, and economic policy, and has contributed to several New York Times best-selling books. His op-eds are regularly published in the New York Times, Wall Street Journal, Washington Post, and other leading publications. His economic policy expertise is cited hundreds of times annually by reporters and columnists in top newspapers and magazines.

My interest in federal spending and the budget deficit started at home in middle and high school. My father was not an economic guru, but a social/fiscal conservative, engineer, and entrepreneur intrigued by these topics leading up to and after the 2008 great financial crisis. He generally felt that John Adams was the greatest of the founding fathers, The Fed and Central Banking model was evil, and Obama was a socialist or the antichrist (not necessarily mutually exclusive scenarios). It was common for weeknight dinner conversations to include how the RINO Republicans and fiscally loose Democrats were unapologetically willing to forgo austerity in return for short term power grabs and political games.

I was 13 years old when Lehman declared bankruptcy, severely impacting my father’s small businesses and our family’s livelihood. I had no idea what that meant as a teenager focused on school, sports, and girls but I could understand there was a misalignment of incentives at the top levels of government. Fast forward 16 years and the situation has only gotten worse. The worrisome spending habits greenlit in 2008 morphed into a full-blown contagion during the pandemic where the Biden administration and Congress pushed over $4T of federal spending allotments during peacetime. This is not a partisan manifesto, both parties act hypocritically on these topics depending on which side controls the Legislature and Executive branch (cue Trump’s parrots this week saying the debt limit needs to be removed after campaigning on fiscal austerity).

In 2017 I was nearing the end of my undergrad studies where I focused on life sciences, I was first introduced to Ray Dalio’s writing via his book, Principles. It was gifted to me after some of my family members noticed my interest in business and financial topics outside my university courses with books like Good to Great, A Random Walk Down Wall Street, and Too Big to Fail. There are many well-founded critiques of Ray Dalio broadly, and Bridgewater Associates specifically, but at the age of 20 without a formal business education I found his writing style to be a great tool for building a framework about how the macro environment is analogous to the water in which we all swim (thank you David Foster Wallace).

We hear doomsday economic forecasts thrown out in headlines like there are shadowy, demonic forces lurking in the underworld patiently waiting for the right opportunity during an economic hiccup to reach up from the great abyss, grab the economy by the ankle and yank it down into oblivion, never to be heard from again except for history books of a formerly great empire. In reality these situations play out across years and happen in two ways according to Mike Campbell from Ernest Hemingway’s The Sun Also Rises. Gradually, and then suddenly.

Dalio published two more books in 2021 and 2022 called Principles for Dealing with the Changing World Order and Principles for Navigating Big Debt Crises, respectively. I promise I do read other economic historians but I find Ray’s work in this particular topic sound. The two books propose frameworks for modeling how big debt crises can play out and the various demographic, economic, financial, political, and technological factors that contribute to the rise and fall of great empires. Both books are worth a read. Suffice it to say that it is becoming more unlikely the United States will make the prudent choices. There are always opportunities to right size the situation throughout the years of buildup and, more often than not, policy makers ignore the wise choice. Put simply, austerity does not get you elected and politics tends to attract the kind of person who will cling to power at the cost rational or economic logic.

This brings us back to Brian Riedl’s lecture. The United States is quickly becoming ensnared in fixed liability obligations. Interest payments on the national debt, Social Security, and Medicare will soon represent the majority of federal spending, creating a debt and fixed liability snowball scenario where all discretionary spending programs get squeezed out of the federal budget. I find this topics particularly timely as Elon Musk and Vivek Ramaswamy embark on their 18 month journey with DOGE to sift through and weed out government bloat, waste, and corruption. While I agree that it is a good thing to shine a light on the inevitable inefficiencies and waste that do exist, I fear they will find no amount of discretionary budget cuts will get us out of the hole we find ourselves.

I thoroughly enjoyed Brian‘s presentation and asked for his permission to share it here. All of the pictures are Brian’s work, and the accompanying remarks are a combination of Brian’s commentary and my notes. I hope you find it as compelling as I do.

Without further ado…

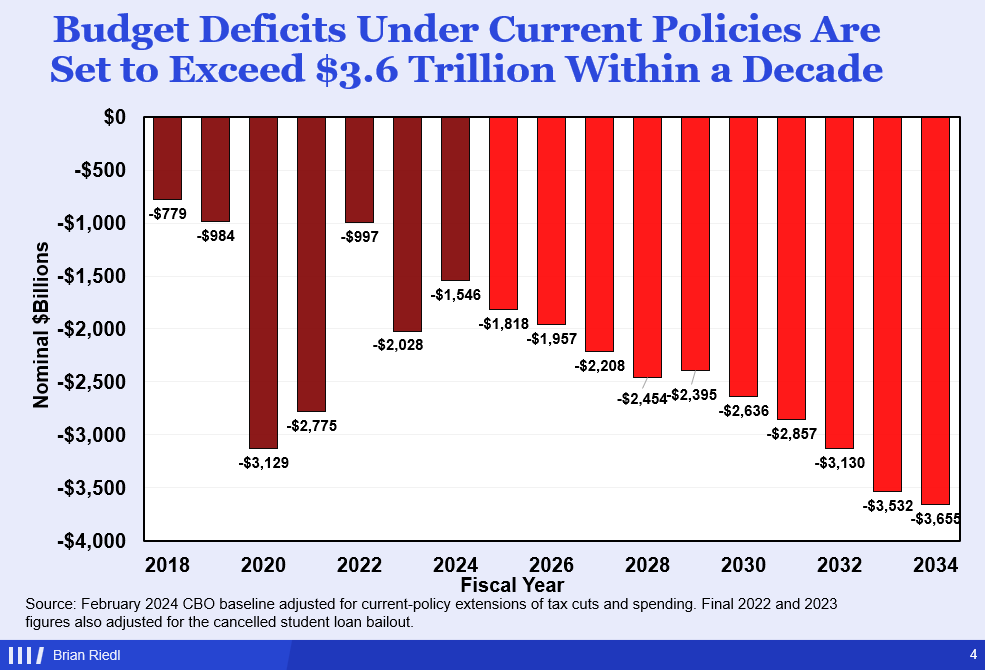

This is the federal budget deficit by year from 2018 projected through 2034. What you will notice is deficits were heading towards about $1T a year until the pandemic, and they went to $3T. Thankfully, the pandemic ended and deficits dropped back to $1T.

Last year (2023), the deficit doubled from $1T to $2T, which rattled economists because the deficit doubled during peace and prosperity (for those taking notes, this is bad). It was the biggest deficit jump ever during peace and prosperity, and it put the deficit at 7.5% of GDP, the biggest deficit ever outside of more than an economic recession. Unfortunately, the problem is only going to get worse. The deficit is expected to drop a little bit this year (2024) towards $1.5T and then, if you assume current policies forward, we will face a deficit of $3.7T in a decade.

This assumes no wars, no recessions, no natural disasters, and low interest rates. The rosy scenario is a $3.7T federal deficit if nothing bad happens and no new spending is passed over ten years.

Here is a look at government spending and revenues as a share of the overall economy. This is how economists usually like to measure these things to see what the country can afford. Historically, The U.S. has spent ~20% of GDP and taxed ~17% of GDP. So historically, we have had deficits of ~3% of GDP. We had a temporary budget surplus from 1998 to 2001, but over the next decade, we are projected to reach a federal deficit of 8.8% of GDP, slightly below long-term average revenues, and increasingly above long-term average spending.

There are no if’s, and’s, or but’s. 8.8% of GDP during peace and prosperity is not great.

The key number for economists is the total debt as a share of the economy. The debt hit 106% of GDP during World War II. Thankfully, World War II ended. And then we got it down to about 40% of GDP, courtesy of being the world’s superpower after victory and exporting democracy. The debt averaged 40% of GDP from pretty much the 1950s until 2008. Since 2008, we've increased towards and eclipsed 100% of GDP. The debt is now bigger than the economy and is only going to get worse.

According to the Congressional Budget Office, the current law baseline gets us to 166% of GDP, conservatively assuming the Trump first term and Biden term tax cuts expire. That assumes all this government spending expires. If you assume spending and revenues continue on their current course (the more likely scenario) then you reach debt to GDP levels of 236%. Then, we get to interest rates. The CBO assumes the interest rate of the debt never goes above 3.8%. If it goes to 4.8% or 5.8% then we are facing a debt to GDP ratio of 250% to 350% of the economy.

Keep in mind what happens if interest rates rise. This chart outlines interest on the debt. You will notice that in the past three years (2021 - 2023), it's gone from $352 billion to $659 billion as interest rates rose. So, we are already paying $347 billion more interest than two years ago. Look where it's going. We are headed towards $1.8T a year in interest payments a decade from now. This is the part of the budget that will not fund a single social security benefit, a single troop, a single veteran or build a single road. $1.8T a year, just on interest. But people can easily get lost in trillions so it’s useful to frame this in another way.

So let's look at what share of your taxes are going to interest on the debt. Previously, it was about 10%. In a decade, more than a quarter of taxes will go towards interest on the debt. That means that when you're working 10 years from now, all the federal taxes you pay from January 1st to April 1st will just be put towards interest payments. On April 1st, finally, your taxes will actually pay for government services United States citizens and allies.

This chart shows each spending category as a share of GDP from 2000 to 2050. What you see with the red line is interest spending as a share of the economy. Interest spending last year surpassed Medicaid. This year, interest will pass defense. Defense is about 3% of GDP. In four years, interest will pass Medicare, which is about 4.2% of GDP. By 2042, interest will surpass social security to be the biggest program in the entire federal budget. And then it just keeps on going.

By the way, in case you might have forgotten, all of this is the rosy scenario we mentioned before. No new wars, interest rates below 3.8%, no pandemics, no natural disasters, no additional government spending.

Consider this. The debt as of April 2024 held by the public is about $27.5T. Over the next 30 years, we will have to borrow cumulatively somewhere between $120T and $150T just to keep our current programs. Again, you're at $27.5T right now. We will have to borrow $120 to $150T.

This begs the question. Who is going to lend to us? Who is going to lend the federal government $120T to $150T? China and Japan hold about $1T each and they are actively trying to dump our debt. The federal reserve bought up a couple trillion during the pandemic. They're also trying to get rid of it. There are other lenders for a little bit of that portion, but for the most part, China and Japan and the Fed cannot swallow $120T to $150T.

And we can discuss Modern Monetary Theory, which is basically the federal reserve taking on the whole thing. That means that American lenders are going to have to supply $120T to $150T. Banks, mutual funds, insurance funds, state and local governments. How feasible is it for them to have that much money to lend the government? And if so, what's going to happen to interest rates? All of this will put huge upward pressure on interest rates, and that's where the real fun begins…

This is the average interest rate on the federal debt. The red line is the nominal rate. The blue line is adjusted for inflation. Let's focus on the red line. 2.5% in 2023.

Here's the danger. The Fed and the Congressional Budget Office believe that interest rates are only going to go to 3.8% over the next 30 years. Which would still be far lower than its been during most of the last 40 years. Is that realistic that the interest rate on the debt is never going higher than 3.8%?

Make it stand out

Is it safe to bet the outcome of the economy on the hope that interest rates remain below 4% forever? When interest rates were 1% and 2%, Washington never locked them in. They're like a subprime borrower. Brian was screaming at policymakers three years ago. He was testifying before Congress on this specific topic and said, “why won't you lock in the low rates for 30 years”? Their answer was because they felt the rates might go lower. Well, now rates are higher and we need to roll over $8T of existing debt over the next 12 months into these 4.5% rates. If rates rise, oh boy.

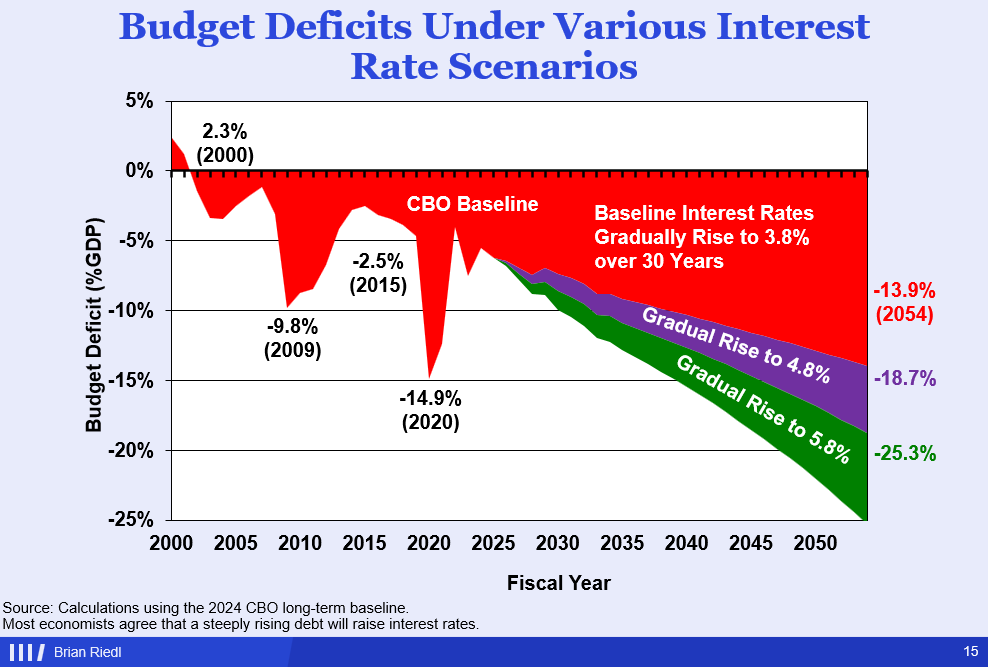

Again, CBO says interest rates are going to be about 3.5% for the next decade. And an earlier chart showed you the $3.6T deficit. Well, if interest rates gradually rise to 4.5%, you're looking at a $4.1T deficit. If interest rates go to 5.5%, you're looking at a $4.7T deficit. Again, if you’re taking notes at home that is not good.

Here's the projection of the budget deficit over the next 30 years. Reminder, you want to aim for a deficit no bigger than 3% of GDP. That will stabilize the budget. If the debt is growing faster than the economy, you're running into unsustainable territory. Ideally, you want to be below 3% deficits.

The baseline budget estimates project an almost 14% deficit. With higher interest rates, you could be running budget deficits up to 25% of GDP per year. This is like economic collapse stuff. Broadly speaking, what we have done as a country and what Congress has done is bet the long-term economy and federal budget on the hope that interest rates never rise again. There is no backup plan for how to handle this much debt with interest rates higher than 2% to 3%.

Lest this all sounds like some poor chap promoting doom and gloom, a group of Wharton economists tried to model out the economy for the next 30 years under current debt plans and current economic policies last October. Their conclusion was their economic models crash when trying to project future macroeconomic variables under current fiscal policy. The reason is that current fiscal policy is not sustainable and forward looking financial markets know it. So what they say is in their economic models, they have to assume massive spending cuts or tax increases for their models to work. You can't even model out the economy without massive spending cuts or tax cuts.

So how did we get here? Let's look at spending. This is the share of federal government spending since 1962. The first thing you might notice is defense. Defense has gone from half of the federal budget to an eighth. That's not driving us off the cliff. Antipoverty is up from 3% to 19%, but look at Social Security and Medicare. Medicare didn’t exist until 1965, but that part of the budget went from an eighth to a third of federal spending over 60 years.

In 2000, we famously had a budget surplus. In fact, in 2000, one of the core policy issues of the Bush vs Gore presidential race was how we should spend all of the federal surplus. Back then, the surplus was 2.3% of GDP. Today, the deficit is 7.5%. So that means the fiscal level declined by 9.8% of GDP since 2000. What happened?

Since 2000, revenue has fallen by 3.5% of GDP. About 2% of GDP in tax cuts. And all 1.5% of GDP from economic factors. Spending jumped 6.3% of GDP. And nearly all of that was social security, health care, and other spending. So, revenues are part of it. Spending is much bigger. For the most part, entitlements drove us from surplus to deficits compared to 2000 levels.

We've also had a big spending spree over the last couple of years. In President Biden's first 20 months, his initiatives signed into law, $4.8T of federal spending over 10 years. You have the American Rescue Plan, the omnibus bill, the infrastructure bill, the Honoring our PACT Act (for veterans), SNAP, the CHIPS Act, etc. As a result, the deficit is in worse shape now than it was when Biden took office.

President Biden likes to say he cut the deficit. Well, the blue line was the baseline deficit path from the CBO office in 2021.The red line is CBO's baseline deficits now. You can see it’s jumped from ~$1T a year now towards $1.5T - $2T annual deficits.

As bad as the last couple of years of have been, this is really a story of social security and Medicare.

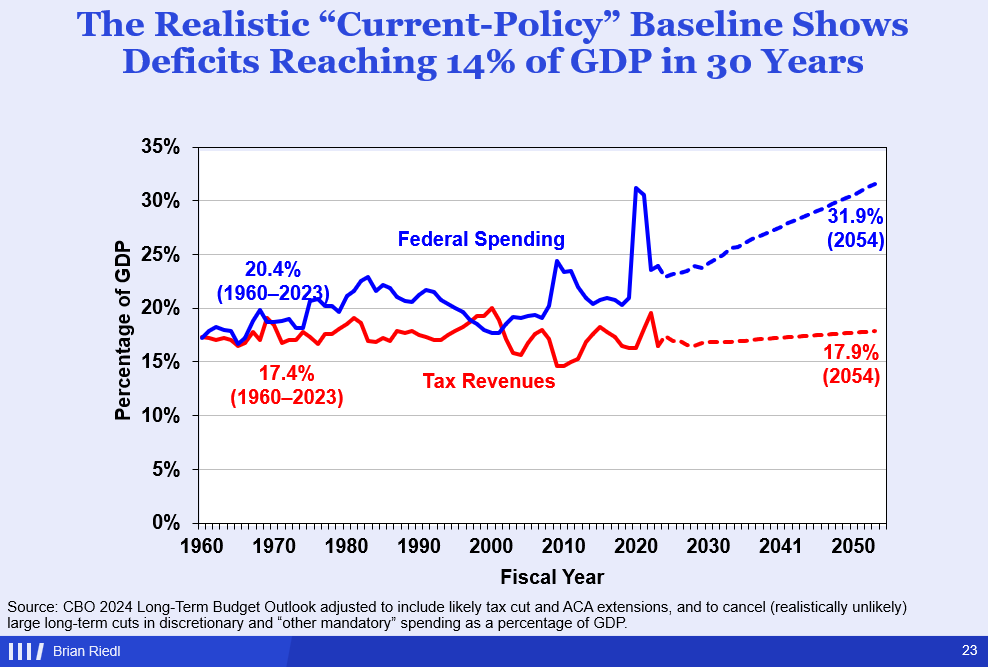

This is the outlook. Remember earlier you saw this chart ending in 2034. Now let’s extend it out to 2054 based on CBO and OBM models. Long term, revenues are going to be steady. Revenues were historically 17.4% and they'll be 17.9%. This accounts for the tax cuts continuing keeping today’s spending programs.

But look at the blue line. It's going towards 32% of GDP. That means a deficit of 14% of GDP. So really, the big variable here compared to historical norms is spending.

Now let’s take the exact same chart and fill it in with spending by category. This is the federal budget from 1960 projected through to 2054. The black line snuck in if you look closely is government revenues.

What you should notice here is social security and healthcare entitlements costing ~14% of GDP by 2054. These are driving interest because interest is resulting from the debt caused by not paying for these programs. So, everything else is getting cheaper long term. It's entirely social security and healthcare.

With this in mind, we need to look at social security and Medicare themselves. This data is for an average income married couple turning 65 next year.

In present value dollars, they will have paid $783,000 into social security over their career and get $831,000 back. Look at Medicare. The average retiring couple is going to receive Medicare benefits triple what they pay it in. Now, multiply that by 74 million baby-boomers retiring. This is going to lead to a worker to a retiree ratio of 2:1 by the 2030s. That means a decade from now. You and your spouse are going to have to support yourselves, your children if you have them and your very own retiree. Every married couple is going to have to pay for their own retiree. You multiply that by 74 million baby-boomers and you have a serious problem.

This chart is the 10-year deficit projection. If you look at the red section you will see what's driving most of it. People will incorrectly tell you how Social Security and Medicare are completely paid for. Put simply, they are not.

Your payroll taxes and your premiums do not fully pay for social security and Medicare. Every year the federal government has to transfer money from the general fund to close the gap. This year the federal government will transfer $650 billion. A decade from now it will have to transfer $2.2T into social security and Medicare benefits. That's your ball game. That's why the deficit is what it is. Everything else is pretty stable.

By the way, none of this is the fault of the seniors. This is not the fault of the people who paid into Social Security and Medicare. They did nothing wrong. They played by the rules. They funded their benefits. They are expecting their benefits back. They did nothing wrong. The problem is simply the demographics of the economy made these programs unsustainable long term. If you want to blame the baby boomers for anything, perhaps you could make an argument for not having enough kids. If they each had 8 or 9 kids, maybe these programs could be maintained.

The congressional budget office projects over $115T in debts over the next 30 years. But this number is a conservative underestimate because it assumes the current tax benefits expire. This is an interesting chart that says over the next 30 years, Social Security faces a deficit of $37T. Medicare faces a deficit of $87T and the rest of the budget is in surplus. So it's pretty clear what's driving the problem.

To dive into these programs individually over the next 30 years, Social Security will take in $74T and pay out $94T plus create an additional $16T in interest payments.

Medicare is significantly worse. It will take in $28T in revenues and pay out $115T in direct outlays and interest costs.

As a percent of GDP over the next 30 years, these programs are going to take in 6% of GDP while their benefits are going to increase up to 11.3% of GDP. If you had taken the interest on the debt directly resulting from these two programs, they will cost 17.6% of GDP.

This means these two programs will be running a shortfall effectively of 11.3% of GDP by 2054. Two single programs.

At that point, again, you will have social security and Medicare costing 11.3% of GDP more than they take in. The rest of the budget is surplus. So what do we do?

If you listen to a lot of Republicans, you will hear them make empty promises about balancing the budget in 10 years without raising taxes, and then they go on a spending spree when they are in office. They will put out press releases saying we are going to balance the budget in 10 years. You can't balance the budget in 10 years. If they say we're going to balance the budget in 10 years without touching tax cuts, you have to get rid of a third of every program.

Of course they say, oh, we're not going to touch Social Security and Medicare. Well then, now you must eliminate 63% of everything else. No one wants to touch veterans, and for good reason. Okay, now you need to take 73% of everything else. Defense cannot be on the chopping block either. Great, well now it is mathematically impossible to balance the budget.

We don't have to balance the budget, it's not the right goal. The target should be to stabilize the debt at 100% of GDP, which it was at until the pandemic blew the doors wide open.

What matters most is the debt’s share of the economy. As the economy rises, the debt can rise proportionally. Just like when your income rises, you can take on a bigger mortgage proportionally. If you stabilize at 100% of GDP, then with interest rates of 4% to 5% the math gets easier. At that level you can maintain 4% to 5% of GDP on interest and it will be stable.

To reach that target, you need the economy and the deficit to grow by similar amounts. You can run a deficit of about 3.6% of GDP per year. Which is still hard compared to a baseline deficit going to 8% and then 14% of GDP. At least under this target you can still run a deficit of $1T to $1.5T a decade from now compared to the baseline from earlier of 3.6$T and 18% of GDP. This is what lawmakers need to have tattooed on their arms. This is what CBO committee members need to testify about in front of Senate and House hearings. This is the target to shoot for. Keep the debt at 100% of GDP.

Getting there is going to be really difficult. This is a table that takes a while to go through but it can be a fun game.

People will say, “Let's just raise taxes. We can close the whole gap by raising taxes.” If you want to stabilize the debt, the gap you need to close gradually rises to 5% of GDP over the next 25 years into the 2040s, not accounting for interest. You have to find 5% of GDP in tax hikes and spending cuts, not accounting for interest.

Well, here's a menu. Try to hit 5% of GDP.

The tax the rich stuff is really hard. The Bernie Sanders wealth tax gets you 0.6% savings. If you want to jack the corporate rate all the way back up to the highest in the world, OK, you get 0.6% savings. Tax capital gains and dividends at 37%? Well, then you can save 0.17% of GDP. Tax financial transactions, 0.1%? That will get you 0.1% of GDP savings.

It's really difficult to get the 5% of GDP by taxing the rich. Really, it's the top three that are the big ones and those are the middle class taxes. Increase payroll tax 10 points, income tax 10 points, and VAT 20 points and you will surpass your goal. You could increase payroll by ~8 points and maybe a 10 point VAT, or maybe 20 point VAT and an 8 point payroll hike. Is that what you want? That's a lot to ask.

Brian’s prediction for where this ends is, ultimately, something like a 10% VAT and an 8% higher payroll tax in 20 to 30 years. That is basically how Europe funds their governments. The difference between us and Europe is that Europe taxes its workers to death in order to give the money back to the workers. They get childcare, family leave, education, health care, cheap college, etc. In the United States you will be paying all those taxes to transfer it to the senior citizens. The workers drowning in the taxes will not be getting the benefits. At least not until you retire.

But this is a fun chart to just kind of sit and ponder. See if you can hit the number 5% of GDP savings number by just taxing the rich. It’s hard.

Ultimately, this is what we will be forced to address. This is inflation adjusted spending levels from 2008 projected through 2034.

For Elon and Vivek fans, yes, look for savings in defense when you can. Non-defense discretionary spending, absolutely, look for savings. What makes this so hard is because most of the growth here is veterans benefits that no one really wants to cut back. You can try to find decent savings here, but really this is where you're going.

The United States faces serious fiscal challenge that extend far beyond typical partisan rhetoric about government waste or inefficiency. The mathematical reality is stark: we are heading toward debt levels between 236% and 350% of GDP, with interest payments potentially consuming 50-80% of all tax revenue. This isn't a distant theoretical problem - it's already manifesting in our current deficit, which doubled to $2 trillion in 2023 during peace and prosperity.

Three critical factors make this situation particularly concerning:

Demographic Reality: The approaching 2:1 worker-to-retiree ratio means every working couple will essentially need to support their own retiree through Social Security and Medicare programs that are fundamentally underfunded. This isn't a failure of seniors who played by the rules, but rather a structural demographic challenge that politics has failed to address.

Interest Rate Vulnerability: We've bet our economic future on perpetually low interest rates, with no backup plan for rates above 3.8%. Even modest increases could trigger a vicious cycle where higher rates lead to larger deficits, requiring more borrowing at even higher rates.

Funding Gap: The sheer scale of future borrowing needs ($120T - 150T over 30 years) raises serious questions about who will lend this money. Traditional buyers like China and Japan are reducing their holdings, and domestic lenders would need to dramatically increase their purchasing of government debt.

The most realistic path forward likely involves stabilizing debt at 100% of GDP through a combination of tax increases (possibly including a VAT and higher payroll taxes) and spending reforms. However, this will require political courage that has been notably absent from both parties. Without meaningful reform, we risk discovering exactly how that "suddenly" phase from Mike Campbell unfolds in the world's largest economy.

What makes this particularly concerning is that discretionary spending cuts alone cannot solve the problem. Even eliminating all government waste and inefficiency - while worthwhile - would be insufficient to address the fundamental imbalances in Social Security and Medicare that will consume an ever-growing share of GDP.

The soaring national debt absolutely matters, and its resolution will likely define the economic future of the next generation of Americans.

Thank you reading. Let me know your thoughts.